In today's rapidly evolving financial landscape, sending and receiving money involves far more than just a simple click of a button. Behind that action lies a complex web of infrastructures, each with its own unique costs, speeds, compliance requirements, and user experiences. Understanding these different payment models is crucial for anyone involved in finance, whether you're an investor, entrepreneur, or just a curious reader.

Let’s delve into the four main models shaping global payments today—each with its distinct advantages and drawbacks.

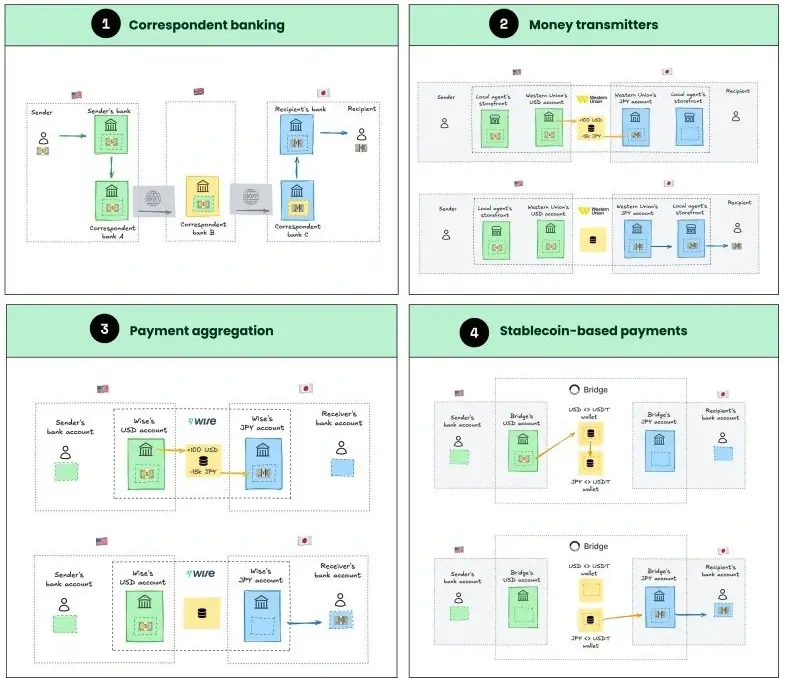

1. Correspondent Banking: The Traditional Backbone

Overview

Correspondent banking, often associated with the SWIFT system, has been the cornerstone of international money transfers. Banks utilize a network of intermediaries that hold accounts with each other to facilitate transactions.

| Pros | Cons |

|---|---|

|

|

This model continues to serve corporates and legacy institutions, despite its limitations.

2. Money Transmitters: A Faster Alternative

Overview

Companies like Western Union and MoneyGram use local pre-funding and pooling methods instead of moving money across borders. They collect funds locally and pay out from balances already held in the destination country.

| Pros | Cons |

|---|---|

|

|

Many modern fintech players, including Wise and Revolut, have adopted this model for its efficiency.

3. Payment Aggregators: The Fintech Revolution

Overview

Payment aggregators, such as Wise, function as global money routers, linking local bank accounts, foreign exchange (FX) engines, and clearing systems.

| Pros | Cons |

|---|---|

|

|

This approach is increasingly preferred by modern fintech companies aiming to optimize payment processes.

4. Stablecoin-Based Cross-Border Payments: The Future

Overview

Stablecoins represent the cutting edge of payment technology. They enable instant settlement on blockchain networks, providing a new format for cross-border payments without traditional banking constraints.

| Pros | Cons |

|---|---|

|

|

The adoption of stablecoins is rapidly gaining traction, especially in regions like Asia-Pacific, Latin America, and Africa.

The Bigger Picture: An Evolving Landscape

Cross-border payments are transitioning from slow, message-based systems operated by banks to fast, programmable networks facilitated by new technologies. While stablecoins may not entirely replace traditional banking services, they are reshaping the value banks provide in areas such as treasury management, compliance, and liquidity.

Understanding these payment models is essential for anyone invested in the future of finance. As we embrace innovations in payment technology, one thing is clear: the landscape of financial transactions is set for significant change.