Opportunity cost is a fundamental concept in economics that has become second nature to many of us. Yet, the fascinating narrative of its birth during a pivotal theoretical revolution is often overlooked. In this blog post, we will explore the essence of opportunity cost, its historical roots, and its significance in modern economic theory, particularly in the context of the Marginal Revolution.

What is Opportunity Cost?

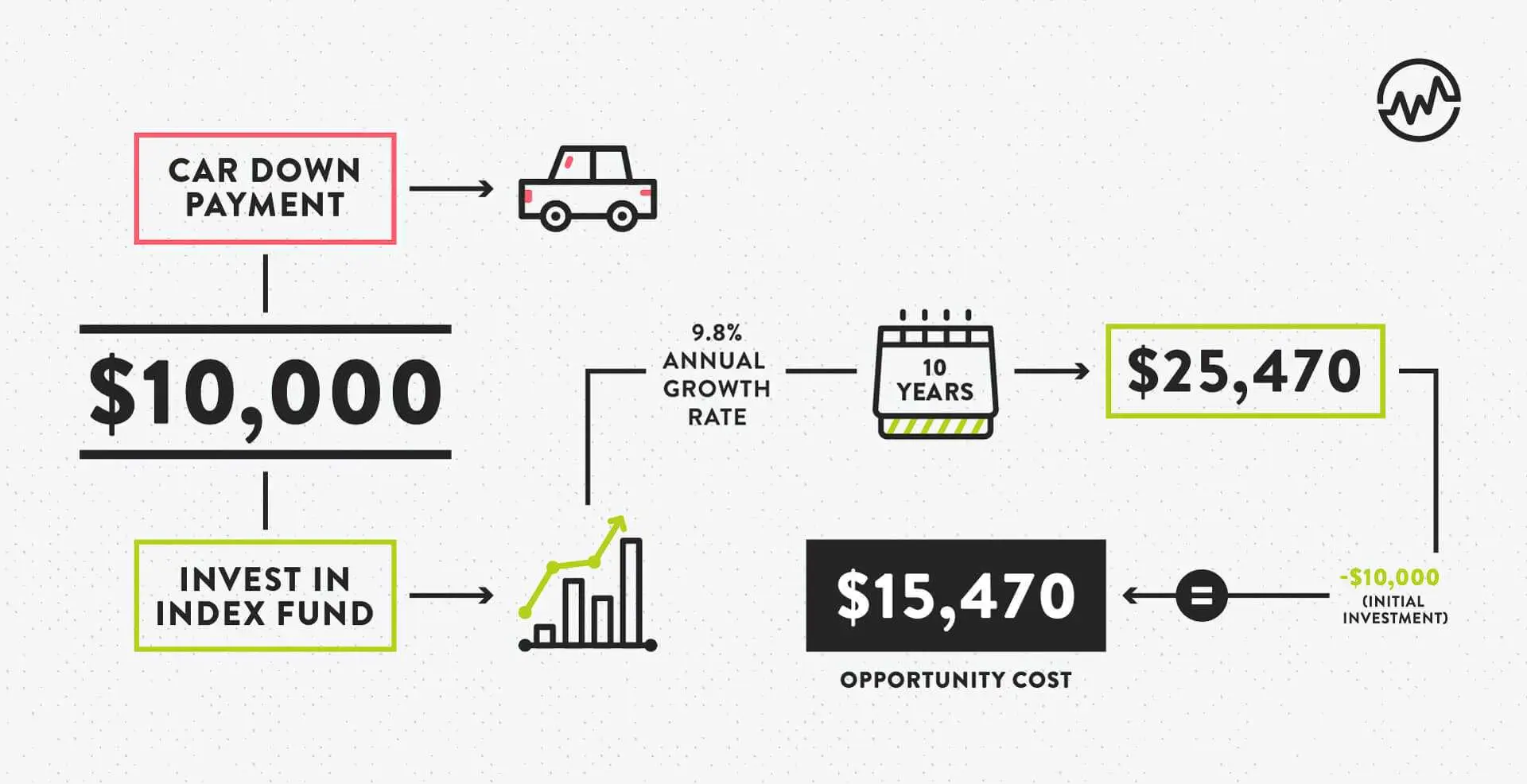

At its core, opportunity cost refers to the value of the next best alternative that must be forgone when making a choice. As defined by renowned economists Paul Samuelson and William Nordhaus in their seminal work, Economics, opportunity cost arises in a world of scarcity. When we choose one option, we inevitably give up others, and the value of those alternatives constitutes our opportunity cost.

This concept is especially relevant in today's resource-constrained environment, where decision-making requires careful consideration of trade-offs.

The Marginal Revolution: A Shift from Classical to Neoclassical Economics

The Marginal Revolution, occurring in the late 19th century, marked a significant turning point in economic thought. Pioneered by economists such as William Stanley Jevons, Carl Menger, and Léon Walras, this movement distinguished neoclassical economics from classical economics.

Henry William Spiegel, in his book The Growth of Economic Thought, highlights this transition, stating that the traditional economic theories of figures like John Stuart Mill lost their relevance as the Marginal Revolution reshaped the structure and methodology of economics. Rather than focusing solely on production and distribution, the neoclassical approach emphasized individual preferences and marginal analysis.

Key Differences between Classical and Neoclassical Economics

| Aspect | Classical Economics | Neoclassical Economics |

|---|---|---|

| Focus | Economic growth, national wealth sources | Optimal resource allocation under scarcity |

| Value Theory | Objective value (labor theory of value) | Subjective value (marginal utility theory) |

| Analytical Focus | Macroeconomic, class analysis | Microeconomic, individual analysis |

| Core Concepts | Division of labor, surplus value | Marginal analysis, supply-demand models |

Scarcity, Subjective Value Theory, and Marginal Analysis

One of the Marginal Revolution's most significant contributions was the introduction of marginal analysis as a formal tool. This framework allowed economists to construct theories around marginal utility, fundamentally challenging classical labor theory.

Classical economists like David Ricardo viewed the creation of wealth as an objective process driven by labor and production. However, they often neglected the subjective nature of value and the diverse desires of consumers. The Marginal Revolution filled this gap by providing a framework for understanding how individuals make optimal decisions under constraints.

Marginal analysis focuses on the utility derived from the last unit of a good consumed, or the output gained from the last unit of input used. This shift laid the foundation for modern microeconomics and reinforced the theory of subjective value.

Carl Menger: Subjective Value, Scarcity, and Opportunity Cost

Carl Menger, a key figure in the Marginal Revolution, emphasized the link between subjective value and opportunity cost. He argued that goods possess value based on their ability to satisfy human wants. When a good is allocated to one purpose, the alternative uses must be sacrificed, highlighting the essence of opportunity cost.

Menger's work, combined with insights from other economists, established opportunity cost as a cornerstone of neoclassical economic thought. Decision-makers must weigh marginal benefits and marginal costs to make informed choices, with each decision reflecting a trade-off where the forgone alternative represents the opportunity cost.

Conclusion

The evolution of opportunity cost is a testament to the ongoing refinement of economic thought. Emerging from early economists' understanding of scarcity and choice, the concept gained clarity and significance during the Marginal Revolution, particularly through Menger's contributions. Today, opportunity cost serves as a foundational element in rational decision-making, emphasizing the necessity of considering trade-offs in an increasingly complex economic landscape.

By understanding opportunity cost, we can better navigate the financial decisions that shape our lives and the economy as a whole.