- Undo

- Redo

- Copy

- Paste

- Delete

- Reload

Joint-University Algo FX Trading Challenge 2021 (Global).

Ideate your trading algorithms, test on a robust back-testing platform, and compete to make a name for yourself!

Gain professional industry knowledge and practical skills to prepare yourself as the next-gen algo-trading professional. All undergraduate and postgraduate students from any faculty at participating universities are eligible.

Create teams of 1~4 members with diverse skills (maths, statistics, finance, coding, presentation) and register by 18 Oct 2021.

Registered teams of 1-4 students will prepare a trading proposal consisting of:

Coding is not required in this round

Submission deadline: 20 Nov 2021

Result announced: 30 Nov 2021

Teams will code their trading algorithm and test on ALGOGENE's back-testing engine, then submit the code

Judges will backtest trading algorithms for return, volatility, robustness and practicality to select advancing teams

Submission deadline: 20 Jan 2022

Result announced: 31 Jan 2022

Each team need to compete in out-sample forward test and live paper trading

Live paper trading will last for 2 months from 1-Feb-2022 to 31-Mar-2022

Teams will present trading plan to judges in a 5-minute pitch session on final day

Judges will select winners in each of these categories:

Final Day: 3 Apr 2022

Form a team of 1~4 members with diverse skills (maths, statistics, finance, coding, presentation) and register by 18 Oct 2021.

Application is closed.

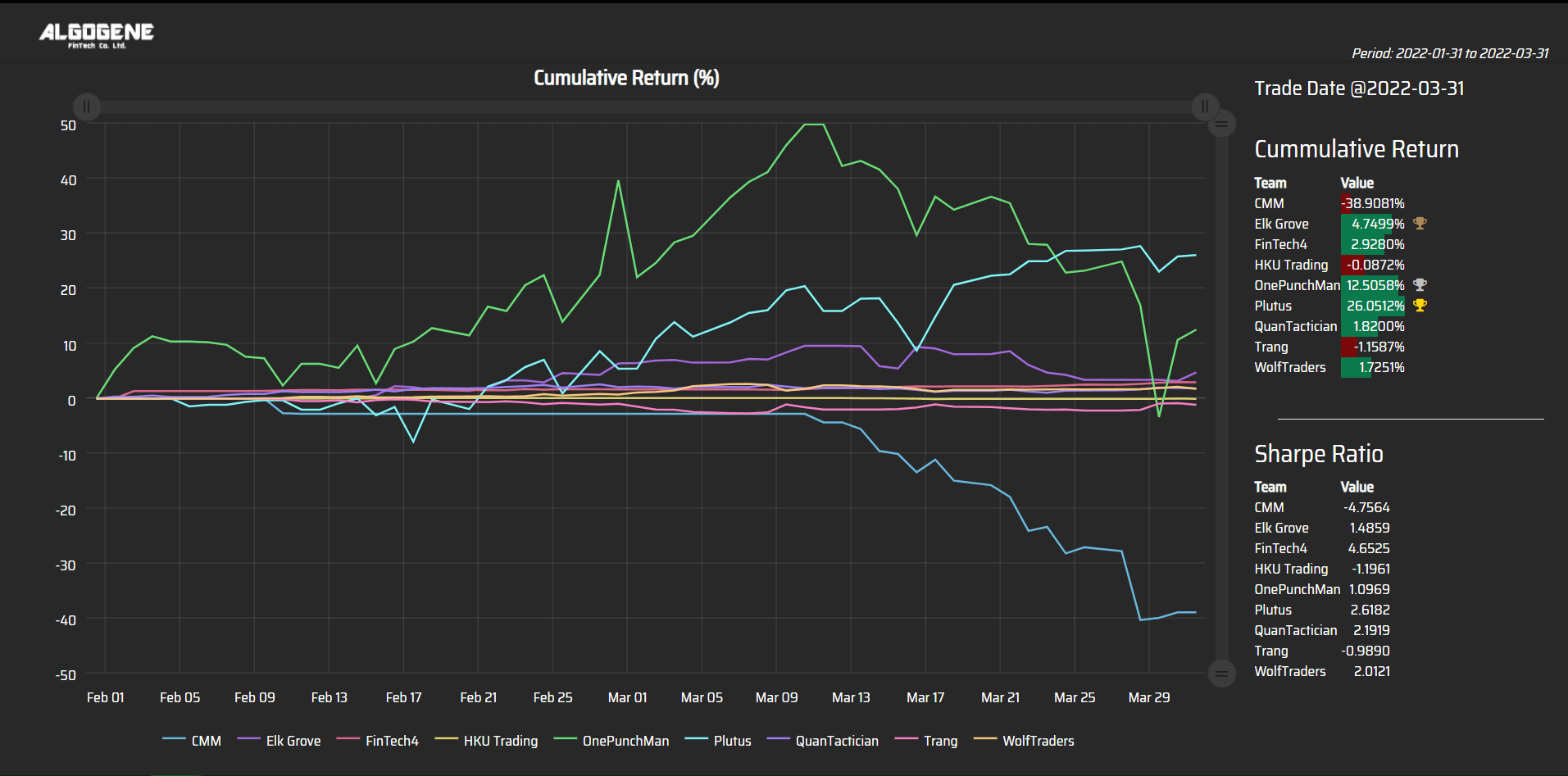

The final result of the Joint-University Algo FX Trading Challenge 2021 (Global) comes out! Congratulation to all winning teams!

Best Return: live trading period 01/02/2022-31/03/2022

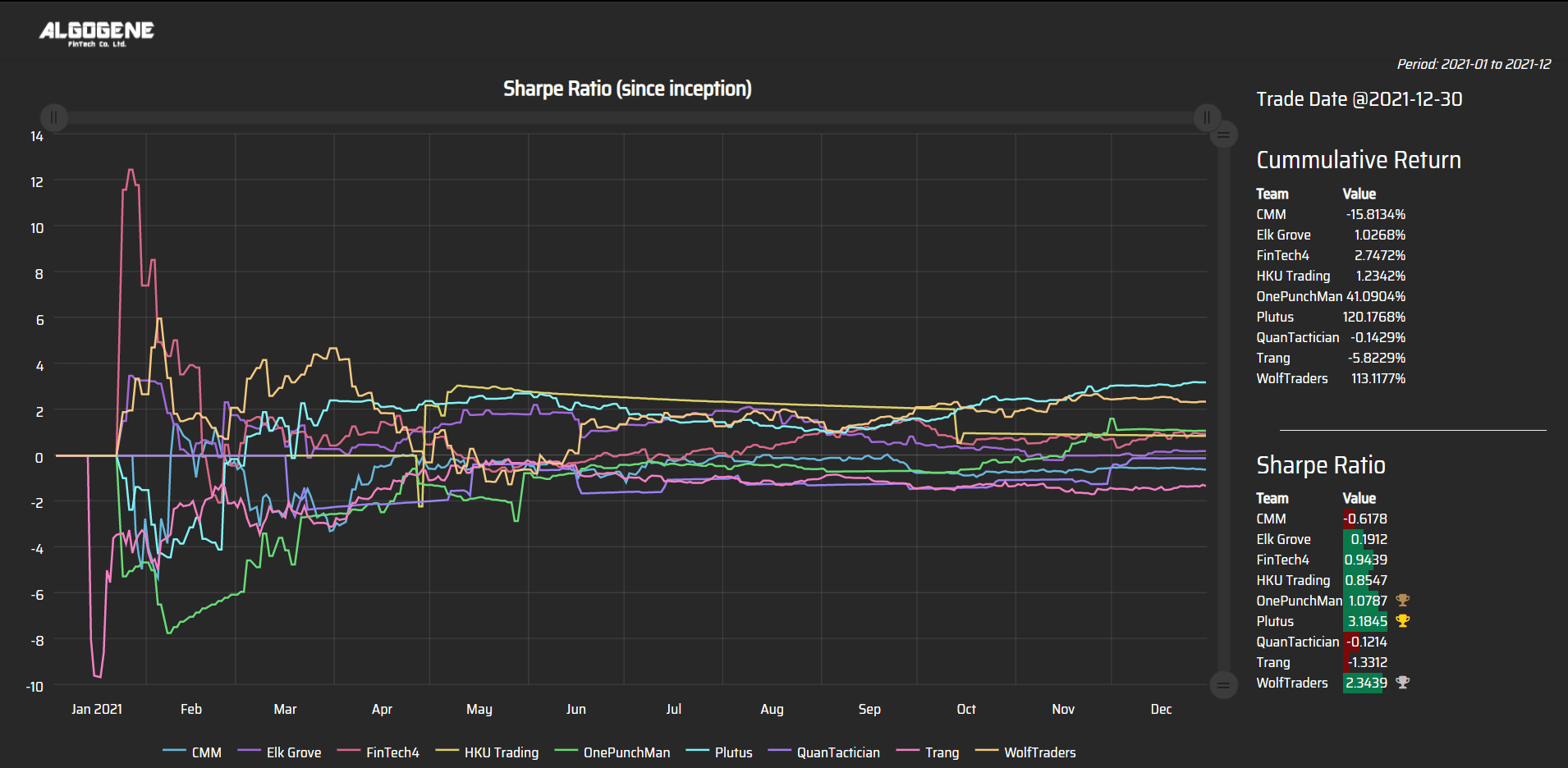

Best Sharpe: 1-year out-sample forward test 1/1/2021 - 31/12/2021

| Rank | Team | Best Return |

| 1 | Plutus (CUHK) | 26.05% |

| 2 | OnePunchMan (CUHK) | 12.51% |

| 3 | Elk Grove (HKU) | 4.75% |

| Rank | Team | Best Sharpe |

| 1 | Plutus (CUHK) | 3.1845 |

| 2 | WolfTraders (CUHK) | 2.3439 |

| 3 | OnePunchMan (CUHK) | 1.0787 |

| Rank | Team | Best Strategy Design |

| 1 | Plutus (CUHK) | LSTM model on portfolio optimization based on daily economic data feed on FX. A day trading strategy using price and fundamental data feed into the pipeline. |

| 2 | Elk Grove (HKU) | Time series mean reversion strategy with long short action based on the spread(bollinger bands or the log spread ratios) on FX. |

| 3 | WolfTraders (CUHK) | BI-LSTM model to make prediction on FX based on news and technical analysis. |

|

演算交易協會舉行第三屆國際聯校外匯算法交易挑戰賽暨就職典禮 中大 Plutus 勇奪3獎成總冠軍 將鑄造成全球首批算法 NFT, 华人头条, Apr 11, 2022 演算交易協會(Algo Challenge Association, 簡稱ACA) 於 4月3日 (星期日)在線上舉辦第三屆國際聯校外匯算法交易挑戰總決賽 (Joint-University Algo FX Trading Challenge 2021 Global)(下稱「比賽」),是全球首個運用區塊鍊及 NFT 技術的算法交易比賽。 ... |

|

演算交易比賽多國學界爭雄 中大生奪冠, 經濟一週, Apr 8, 2022 Algo Trade(演算交易)逐漸為年輕投資者所認識,演算交易協會本月初舉辦際聯校外匯算法交易挑戰總決賽,除了是全球首個運用區塊鍊及 NFT 技術的算法交易比賽,亦是賽事首次對全球所有大學生開放。 |

|

演算交易協會第三屆國際聯校外匯算法交易挑戰賽, am730, Apr 8, 2022 演算交易協會早前在線上舉辦第三屆國際聯校外匯算法交易挑戰總決賽,是全球首個運用區塊鍊及NFT技術的算法交易比賽,以培養下一代算法交易人才,推動不同地區的金融科技行業。賽事首次對全球所有大學生開放,獲全球各地約二百名學生報名參與,其中香港中文大學量化金融一年級生組成的Plutus團隊獲得「最佳回報」、「最佳夏普比率」、「最佳策略設計」各分項比賽冠軍,得獎隊伍們將獲總值$6,300美金作為獎金,並獲得主辦單位的實習或全職工作機會。 |

|

【國際比賽】第三屆國際聯校外匯算法交易決賽 中大團隊奪3獎成總冠軍, HKET, Apr 5, 2022 演算交易協會於2022年4月3日在線上舉辦第三屆國際聯校外匯算法交易挑戰總決賽,為全球首個運用區塊鍊及 NFT 技術的算法交易比賽。由香港中文大學量化金融一年級生組成的 Plutus 團隊獲得「最佳回報」、「最佳夏普比率」、「最佳策略設計」各分項比賽冠軍,隊伍應用 LSTM 模型分析每日外匯消息、宏觀經濟數據,以達致投資組合優化。得獎隊伍們將會獲得總值$6,300美金作為獎金,並獲得主辦單位的實習或全職工作機會。 |

|

第三屆國際聯校外匯算法交易決賽 中大Plutus勇奪3獎成總冠軍, 香港商報網, Apr 5, 2022 演算交易協會(Algo Challenge Association, 簡稱ACA) 於 2022年4月3日 (星期日)在線上舉辦第三屆國際聯校外匯算法交易挑戰總決賽 (Joint-University Algo FX Trading Challenge 2021 Global)(下稱「比賽」),是全球首個運用區塊鍊及 NFT 技術的算法交易比賽。 |

|

The finale of Joint-University Algo FX Trading Challenge 2021 (Global), InvesTalk and ACA, Apr 3, 2022 The first-ever worldwide algo contest applying NFT and blockchain technology. Join us live on 3 Apr, 2pm (HKT) to witness the champion strategy! |